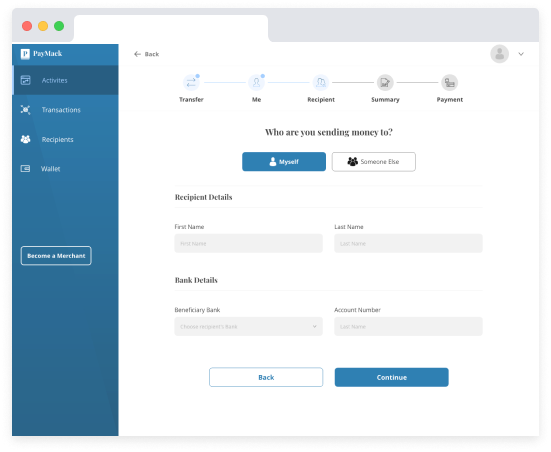

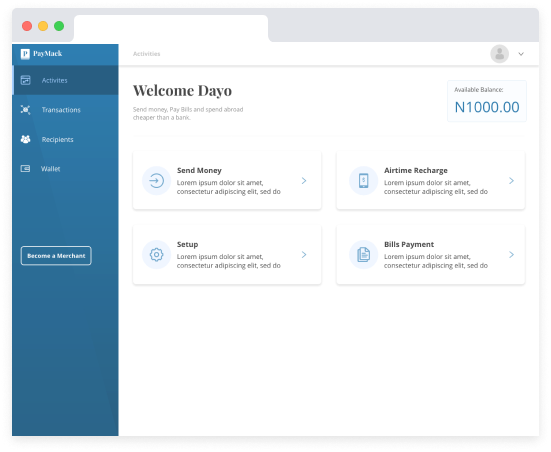

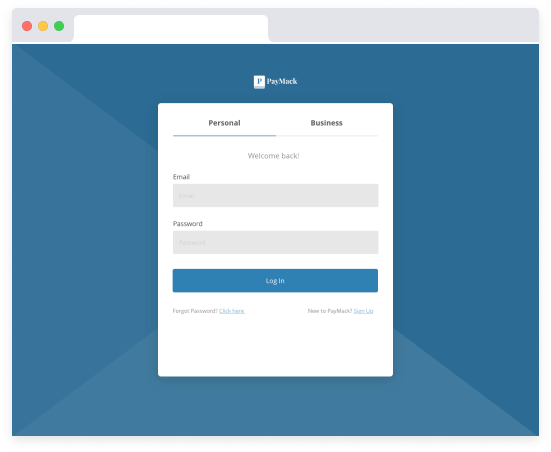

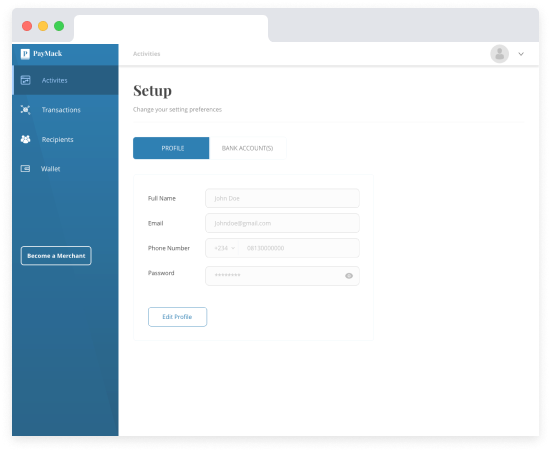

📱 Final Screens

The app, screen by screen

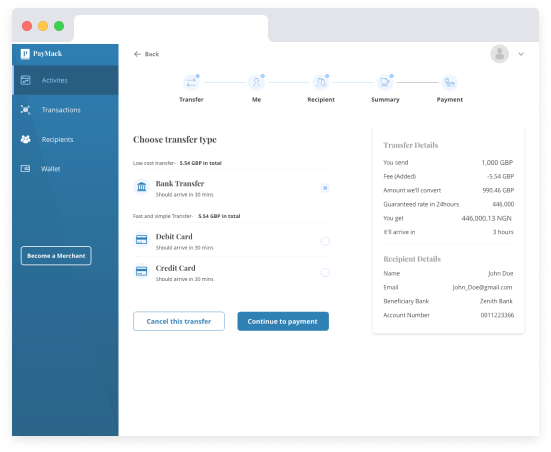

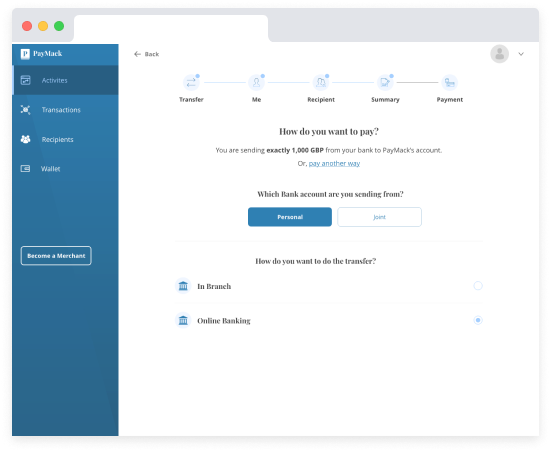

Paymack's final UI, a clean, friction free money transfer and bill payment experience built for everyday Nigerians.

A product design project for Findworka — I designed Paymack, a money transfer and bills payment gateway that removes friction from everyday financial transactions, built for the Nigerian mobile first market.

When I joined Paymack, the company had a bold ambition: one app to replace three separate payment platforms. The business logic made sense. But from a design perspective, I knew that merging transfers, bill payments, and merchant tools into one product without overwhelming everyday users was going to be genuinely hard. Most Nigerians I spoke to had already been burned by fintech apps that were either too complex or too unreliable. Trust was the real problem, not features.

My brief was to design a unified experience where every core action could be completed in 3 taps or fewer, without hiding the power features the business needed to compete. That tension, between simplicity and depth, shaped every decision I made.

Fintech design demands an extra layer of rigour around trust, error states, and recovery flows. Every edge case in a payment flow is a potential moment of panic for the user I mapped all of them before designing the happy path.

Every screen in Paymack was designed around one principle, every user should feel in control of their money, whether they're sending ₦500 or ₦500,000.

Unifying three platforms into one product meant making hard trade offs. These were the decisions that defined the experience.